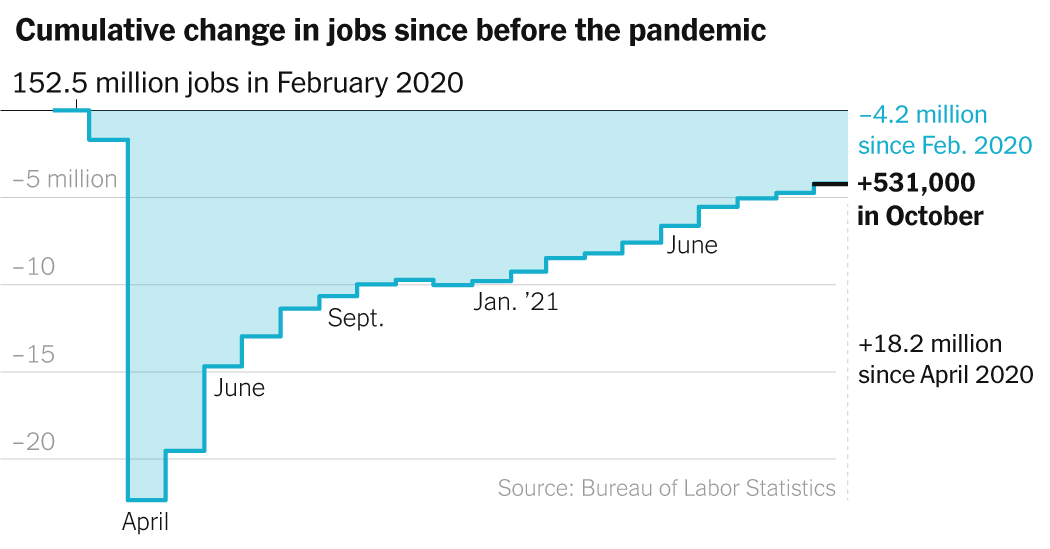

The American economy added 531,000 jobs in October, the Labor Department said Friday, a sharp rebound from the prior month and a sign that employers are feeling more optimistic as the latest coronavirus surge eases.

Economists polled by Bloomberg had been looking for a gain of 450,000 jobs. The unemployment rate declined to 4.6 percent, from 4.8 percent.

The October gain was an improvement from the 312,000 positions added in September — a number that was revised upward on Friday.

Hiring has seesawed this year along with the pandemic, especially in vulnerable sectors like hospitality and retail, where workers must deal face to face with customers. White-collar employees have fared better, since many can work remotely.

Some employers are complaining of a shortage of workers, as many people remain on the sidelines of the job market. The labor force participation rate — the share of the working-age population employed or looking for a job — was flat in October.

In theory, the demand for workers should be drawing more people into the labor force, but the participation rate is nearly two percentage points below where it was before the pandemic. Early retirements have been a factor.

A federal supplement to unemployment benefits expired in early September, and experts are watching whether the end of that assistance — and a depletion of savings accumulated from other emergency programs — increases the availability of workers.

So far, those effects have been muted, as health concerns and child care challenges have continued to affect many families. At the same time, the labor shortage has given workers a measure of leverage they’ve not experienced in recent years.

“For the last 25, maybe 30 years, labor has been on its back heels and losing its share of the economic pie,” said Mark Zandi, the chief economist at Moody’s Analytics. “But that dynamic is now shifting.”

Supply chain problems are another headache for employers. Automobile manufacturers have been particularly hurt by a shortage of semiconductors, while many companies are dealing with rising prices for raw materials and transportation.

The Commerce Department reported last week that the economy grew by 0.5 percent in the third quarter, compared with 1.6 percent in the second quarter. Economists attributed the slowdown to the resurgent pandemic and the supply chain holdups.

Still, there are reasons to be optimistic. The Federal Reserve said Wednesday that it would begin winding down the large-scale bond purchases that have been underway since the pandemic struck, signaling that it considers the economy healthy enough to be weaned from the extra stimulus.

“The labor market is tight,” said Scott Anderson, chief economist at Bank of the West in San Francisco. “Consumers are in good shape, and the willingness to spend is certainly there.”

More Stories

Ronny J and Branden Condy were recently spotted together in front of LIV club in Miami Beach, FL

Abu Dhabi Sustainability Week to host first Green Hydrogen Summit

IDEX, NAVDEX to showcase fast-changing defence sector